What Is an Integrated Resort (IR)? Current Developments in Asia and the Osaka IR’s High-Standard Regulatory Framework and MICE Strategy

An integrated resort (IR) is a large-scale, mixed-use development that combines a range of facilities — including hotels, convention and exhibition venues (MICE), entertainment facilities, and retail — under a unified operational model, with casino revenue forming part of its overall business foundation.

IR are not limited to entertainment; they function as economic and cultural hubs that enhance a destination’s appeal and attract a wide spectrum of visitors for both business and leisure, throughout the day and night. Through this integrated structure, IR developments have been adopted across Asia as a means of driving tourism and stimulating regional economies.

This article provides an overview of the IR planned to open in Osaka in 2030, together with the current landscape of integrated resorts in neighboring Asian markets.

Definition of Integrated Resorts (IR) and Their Business Model

The term “Integrated Resort” (IR) is often associated with casinos. However, its core concept extends beyond gaming. An IR is a large-scale tourism complex that integrates a wide range of facilities, with casino revenue forming part of its overall business foundation.

The expansion of IR development across Asia reflects a strategic objective: leveraging the high profitability of casino operations to develop large-scale tourism infrastructure without relying heavily on public funding, while contributing to regional economic growth.

What “Integration” Means in an Integrated Resort

The defining characteristic of an IR lies in the concept of “integration.” It does not simply refer to multiple businesses being located in the same place. Rather, IR are designed based on a unified master plan, where each facility complements the others and functions as part of a cohesive ecosystem.

This integrated structure aims to enable visitors to complete their entire experience — including consumption and stay — within a single destination, creating a seamless and comprehensive environment.

Core Components of IR and Their Functions

IR are large-scale, mixed-use developments that integrate a range of facilities — including casinos, hotels, convention and exhibition venues (MICE), retail, entertainment, and theme parks — under a unified operational structure. While the casino serves as a central revenue source, IR are typically defined in legal frameworks as comprising casinos, convention and exhibition facilities, accommodation, and other tourism-related infrastructure.

1.Casino Facilities: The Revenue Engine

The casino functions as the primary financial driver of the IR. However, its physical footprint is often strictly limited. In Japan’s IR plan, for example, the casino floor area is capped at 3% of the total gross floor area. Despite this limitation, the high profitability of casino operations supports the development and operation of large-scale facilities — such as MICE venues and theaters — that may not be financially viable on their own.

2.MICE Facilities: A Hub for Business Tourism

MICE facilities, including convention centers and exhibition halls, are essential components of IR, serving as globally competitive hubs for business tourism. Visitors attending MICE events typically demonstrate higher spending levels and are more likely to visit during weekdays, contributing to stable revenue streams for the overall resort.

In the Osaka IR plan, facilities are expected to include a convention hall with a capacity exceeding 6,000 participants and approximately 20,000 square meters of exhibition space, indicating the strategic importance placed on MICE functions.

3.Hotels, Entertainment, and Retail: Enhancing the Stay Experience

Accommodation facilities, particularly luxury hotels, are designed to meet the needs of a wide range of visitors, including business travelers, VIP guests, and families. Entertainment venues — such as theaters, arenas, and theme parks — along with high-end retail and dining, attract visitors beyond gaming-focused segments. These elements contribute to extending the length of stay and enhancing the overall visitor experience.

The Strategic Structure of the IR Business Model

The IR business model is characterized by a dual-revenue structure, in which high-margin casino revenues are reinvested into the development and operation of non-gaming facilities.

This structure enables IR to function not merely as large-scale gaming venues, but as economic and cultural hubs that enhance urban attractiveness and draw diverse visitor segments. A notable feature of IR design is the strategic balance between the relatively small physical footprint of the casino and its significant economic contribution. Although the casino occupies a limited area, it generates a substantial portion of the revenue required to sustain multi-billion-dollar developments.

The Public Policy Role of IR

Beyond private sector profitability, IR are also positioned as policy instruments designed to generate positive externalities for regional economies. Governments grant casino licenses as incentives to private operators, encouraging investment in large-scale tourism infrastructure such as MICE facilities.

Revenue generated from IR operations — including taxes and levies (for example, approximately 30% of gross gaming revenue in Japan’s plan) — is typically allocated to public initiatives such as gambling addiction measures, infrastructure development, and cultural promotion.

Dual Revenue Structure and the Strategic Role of MICE

The IR model relies on redistributing the high profitability of the casino segment — often subject to strict floor-area limitations — to support the capital-intensive non-gaming sector. This financial structure makes it possible to sustain facilities such as hotels, theme parks, and, in particular, MICE infrastructure.

MICE facilities are positioned as core components of IR, functioning as internationally competitive venues for conferences and exhibitions. They contribute to increasing weekday utilization and attracting diverse visitor segments beyond gaming customers, creating a mutually reinforcing relationship between gaming and non-gaming operations.

In the Osaka IR project, the planned convention and exhibition facilities further underscore the priority placed on MICE. At the same time, the allocation of tax revenues and levies to public welfare initiatives highlights the role of IR as part of broader public policy frameworks.

Current Landscape and Historical Context of Major IR Markets in Asia

The IR market in Asia reflects a diverse range of models shaped by each country’s strategy and social context. These include gaming-focused models, quality-driven approaches, tourism-oriented developments, and growth-focused strategies.

Across the region, the competitive landscape is gradually shifting from a primary focus on gaming toward broader non-gaming sectors, including MICE, entertainment, and hospitality.

Macau: Transitioning from a Gaming-Dominated Economy to Diversification

Macau’s gaming industry dates back to its legalization in 1847, and following market liberalization in 2001, the city rapidly developed into the world’s largest gaming hub, surpassing Las Vegas. For many years, Macau represented a “gaming-focused” model, with gaming revenues accounting for more than 90% of total IR revenue. At its peak, the casino industry contributed approximately 63% of the region’s GDP.

However, in response to policy shifts in mainland China, the Macau government has positioned economic diversification as a top priority. Under concession agreements renewed in 2023, all six operators are required to invest a total of more than MOP 118 billion (approximately JPY 1.9 trillion) over the next decade, with around 90% allocated to non-gaming sectors. At the same time, regulations on VIP junket operators have been significantly tightened, accelerating the transition from a VIP-driven model to a mass-market-oriented approach.

Singapore: A MICE-Led Success Model Under Strict Regulation

Singapore introduced IR in 2005 as part of a strategy to revitalize its tourism sector and strengthen its position as a leading MICE destination in Asia. The government adopted a duopoly model, limiting licenses to two operators. Following the opening of Marina Bay Sands (MBS) and Resorts World Sentosa (RWS) in 2010, the country achieved rapid growth, with international visitor numbers increasing by approximately 60% and tourism revenue by around 90% within four years.

A key factor behind this success is the “Singapore model,” characterized by strict social safeguards. Local citizens and permanent residents are required to pay a high entry levy of SGD 150 (approximately JPY 16,000) per visit, aimed at discouraging casual access and mitigating gambling-related risks. In addition, third-party exclusion systems automatically restrict entry for individuals such as bankrupt persons or recipients of social assistance.

More recently, the Singapore government extended the casino exclusivity rights of both operators until 2030, in exchange for requiring additional investments of more than SGD 9 billion (approximately JPY 7 trillion), primarily directed toward non-gaming facilities. Marina Bay Sands plans to develop a fourth hotel tower and a large-scale arena, while Resorts World Sentosa is expanding its theme park and other attractions, further strengthening MICE capabilities and entertainment offerings.

South Korea: Foreigner-Only Casino Model and Competitive Positioning Ahead of Osaka IR

South Korea operates approximately 20 casinos, the majority of which are restricted to foreign visitors, with the exception of Kangwon Land, which is accessible to domestic players. This reflects a “tourism-oriented” model in which casinos are positioned as a tool for attracting international visitors.

In recent years, large-scale IR developments have been concentrated around Incheon International Airport, including Paradise City and Mohegan INSPIRE Entertainment Resort, forming an “airport cluster” of integrated facilities targeting foreign demand.

At the same time, the planned opening of Osaka IR is widely regarded as a competitive challenge for the Korean market. Some analyses suggest that up to 7.6 million Korean visitors annually could shift to Japan, with approximately USD 1.9 billion in spending potentially redirected. In response, South Korea is exploring regulatory adjustments and competitiveness measures. Kangwon Land, the only casino open to Korean nationals, has also announced plans to expand its casino floor area by approximately three times as part of its investment strategy.

Developments in Other Asian Markets

In the Philippines, the government-owned Philippine Amusement and Gaming Corporation (PAGCOR) oversees both regulation and operations. IR development has been concentrated in the Entertainment City district along Manila Bay, contributing to rapid growth that has positioned the country as one of the largest gaming markets in Asia. The Philippines adopts a relatively open model in which domestic access to casinos is permitted.

Vietnam, which traditionally limited casino access to foreign visitors, introduced a pilot program in 2017 allowing local citizens to enter selected properties — such as Corona Resort & Casino on Phu Quoc Island — under strict conditions, including income requirements and entry fees. This “conditional access” model continues to be tested and extended.

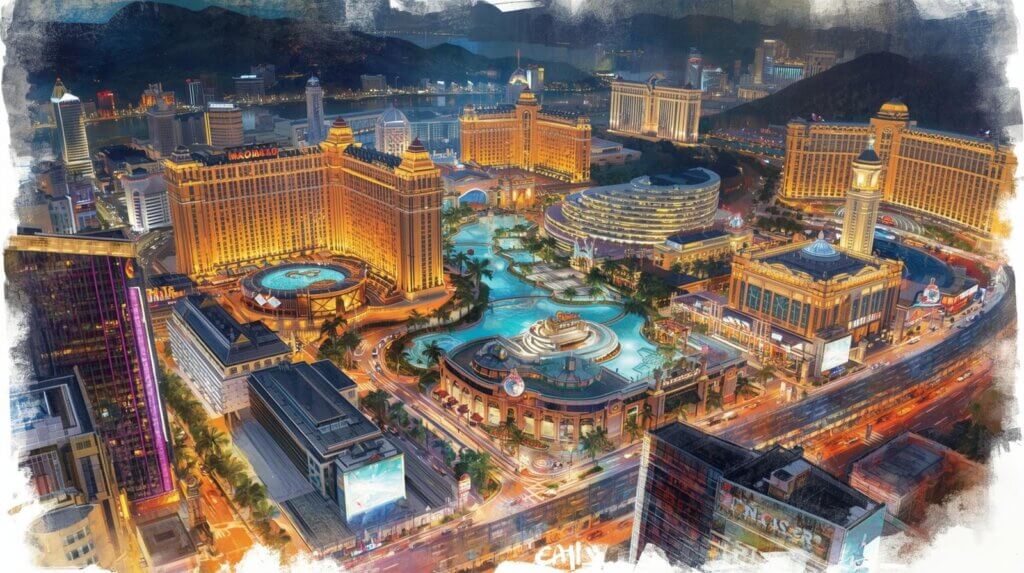

Osaka IR, Japan: Detailed Regulatory Framework and MICE Strategy

In Japan, the IR Implementation Act was enacted in 2018, and in April 2023, the IR district development plan for Yumeshima in Osaka became the first to receive national approval.

Investment and Objectives of Osaka IR

The Osaka IR project will be developed and operated by a consortium led by MGM Resorts International and ORIX Corporation, with an initial investment of approximately JPY 1.27 trillion. The project aims to open by the summer of 2030 and is projected to attract around 20 million visitors annually, generating an estimated economic impact of approximately JPY 1.14 trillion per year in the Kansai region.

A central strategic focus of Osaka IR is the development of a “globally competitive MICE hub.” The project is positioned as an infrastructure investment supporting Japan’s broader tourism strategy. It is required to include large-scale convention and exhibition facilities, venues for showcasing Japanese culture, and entertainment offerings suitable for a wide range of visitors, including families. This reflects its role as a comprehensive tourism and cultural complex rather than a casino-centered development.

A Strict Regulatory Framework for Casino Operations

Japan’s IR framework is considered among the most stringent globally, aiming to balance economic benefits with the mitigation of social risks. While drawing on elements of the Singapore model, the system incorporates additional regulatory measures.

- Casino floor area is strictly limited to within 3% of the total gross floor area of the IR.

- Access for domestic users is regulated through an entry levy of JPY 6,000 per visit (within a 24-hour period).

- Usage frequency is also restricted, with a maximum of three visits within seven days and ten visits within 28 days.

- Strict identity verification is required for Japanese nationals and residents, including the use of the My Number identification system to manage entry records and frequency.

These measures are designed to address concerns related to gambling addiction and public safety. In addition, casino revenues are subject to a levy of 30%, shared equally between national and local governments at 15% each.

Strategic Comparison of Asian IR Markets and Future Outlook

IR policies across Asia can be broadly categorized based on regulations governing domestic access to casinos.

Regulatory Models and Competitive Strategies

Open-access model: Adopted in markets such as Macau, the Philippines, and Malaysia, where domestic visitors are generally permitted entry subject only to age restrictions. While this model can generate significant economic returns, it also carries higher social risk. Macau is currently accelerating efforts to reduce its reliance on this structure.

Conditional access model: Implemented in Singapore, Japan, and Vietnam, where domestic access is permitted under specific conditions, such as entry levies, visit limits, or income requirements. This approach seeks to balance economic benefits with social safeguards, and Singapore is often cited as a successful example.

Restricted access model: Seen in countries such as South Korea (with the exception of Kangwon Land) and Thailand, where casino access is largely limited to foreign visitors. While this model helps mitigate social concerns, it may constrain domestic demand and limit overall economic impact.

Japan’s approach builds on the Singapore model while introducing additional measures, such as stricter visit limits, reflecting a strong emphasis on minimizing social risks.

Intensifying Competition and the Shift Toward Non-Gaming Investment

The planned opening of Osaka IR has the potential to reshape the tourism landscape in Northeast Asia, with particular implications for neighboring markets such as South Korea. In response, investment in non-gaming sectors is accelerating across the region.

Macau is being required to direct substantial capital toward non-gaming development, while Singapore is expanding its facilities in exchange for extended exclusivity rights. As a result, the primary area of competition is shifting away from casino operations toward non-gaming offerings, including entertainment, MICE infrastructure, and service quality.

The Growing Importance of Sustainability and Governance

The Asian IR market is evolving toward a more balanced approach that seeks to align economic benefits with the management of social risks. Ensuring long-term sustainability will depend on robust governance frameworks and the effective implementation of social responsibility measures.

Countries are increasingly leveraging both regulation and technology to strengthen responsible gaming systems, including measures to prevent gambling addiction and exclude criminal elements. For example, Japan’s use of the My Number identification system for entry management reflects this trend.

Considerations related to ESG (environmental, social, and governance) are also becoming integral to the planning and operation of IR developments.

Conclusion

Integrated resorts have evolved across Asia into multi-functional tourism infrastructure, with casino revenue serving as a financial driver while MICE functions play a central role in attracting diverse visitor segments.

The diversification of Macau, the success of Singapore’s MICE-led model, and the strict regulatory framework combined with non-gaming strategies in Osaka IR all indicate a broader transition in the Asian IR market from scale-driven growth to value-oriented development.

As the Osaka IR project moves toward its planned opening around 2030, the Asian IR market is expected to enter a new phase of expansion and competition. Sustained success will depend on the ability to balance economic performance with social responsibility, supported by sophisticated governance and operational capabilities.

-

MICE and the Attention Economy: The Value of Live Events in Competing for Attention

-

【Report】Board Game Business Expo Japan 2026 (BGBE): Western Japan’s Largest Board Game Festival — A Report on the Event That Doubled Attendance to 20,000